In Indonesia’s dynamic financial landscape, banks are navigating increasing complexities, from exposure to natural disasters, ongoing challenges with non-performing loans (NPLs), and the growing importance of serving emerging markets.

To thrive, banking leaders must look beyond traditional data models and embrace Geographic Information Systems (GIS) as a core enabler of decision intelligence. Powered by platforms like Esri’s ArcGIS, GIS is no longer just a “mapping tool.” It has become a strategic capability that integrates location intelligence in banking into every aspect of operations—delivering measurable impact and competitive advantage.

Why GIS matters for Indonesian banking

Indonesia’s geography makes risk management uniquely complex. With thousands of islands, dense urban centers, and communities living in flood-prone or earthquake-prone areas, banks cannot rely solely on traditional credit scoring.

Integrating GIS and geospatial intelligence into banking workflows enables institutions to anticipate risks, optimize portfolios, and expand into new markets.

The urgency is clear: without GIS, banks risk miscalculating credit risk, overlooking disaster exposure, and missing out on emerging markets and opportunities.

With GIS, they gain the foresight and precision needed to build more resilient portfolios.

How banks can utilize GIS

GIS transforms raw geographic data into actionable intelligence that supports both strategic planning and day-to-day operations. Key uses for GIS in banking include:

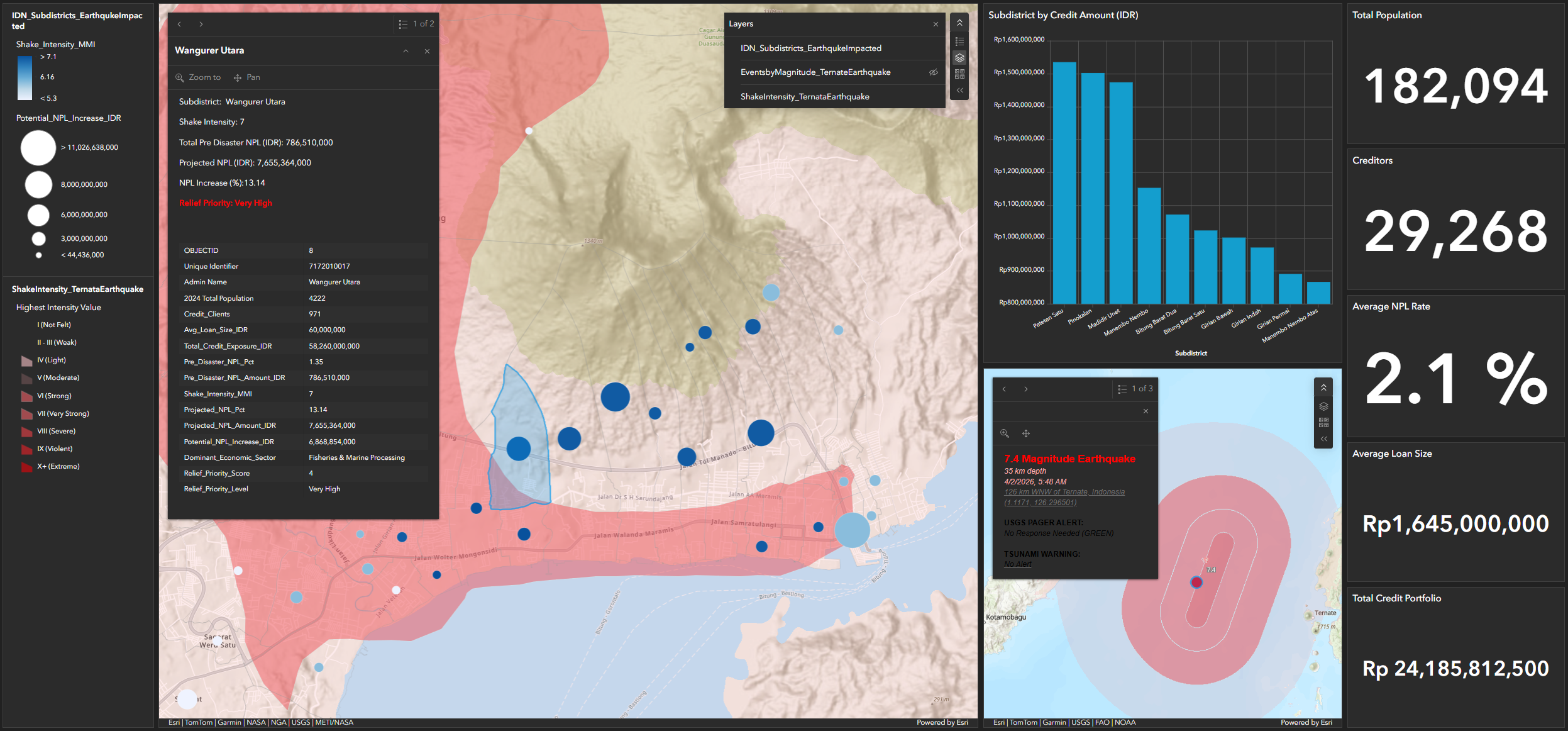

Risk management: Enriching credit risk analysis with disaster exposure

- Geospatial risk indicators: Overlay flood maps, seismic zones, and infrastructure quality with credit portfolio data to refine credit scoring and enrich risk management strategies.

- Local economic proxies: Use employment density and informal sector concentration as credit resilience signals.

- Area-based behavioral insights: Track repayment trends at the districts level for granular risk profiling.

This enables banks to proactively adjust lending strategies in high-risk zones, reducing defaults, and safeguarding portfolios.

Non-performing loans (NPL) management

- Pre-disbursement targeting: Validate borrower eligibility by cross-checking socio-economic data with local living costs.

- Early warning signals: Identify crime or economic shifts that may trigger repayment issues.

- Post - disaster credit rehabilitation strategy: Analyze heavily impacted populations post disasters to forecast at risk portfolios and plan credit relief plans.

GIS strengthens loan monitoring and early intervention, ensuring programs like subsidized housing remain sustainable.

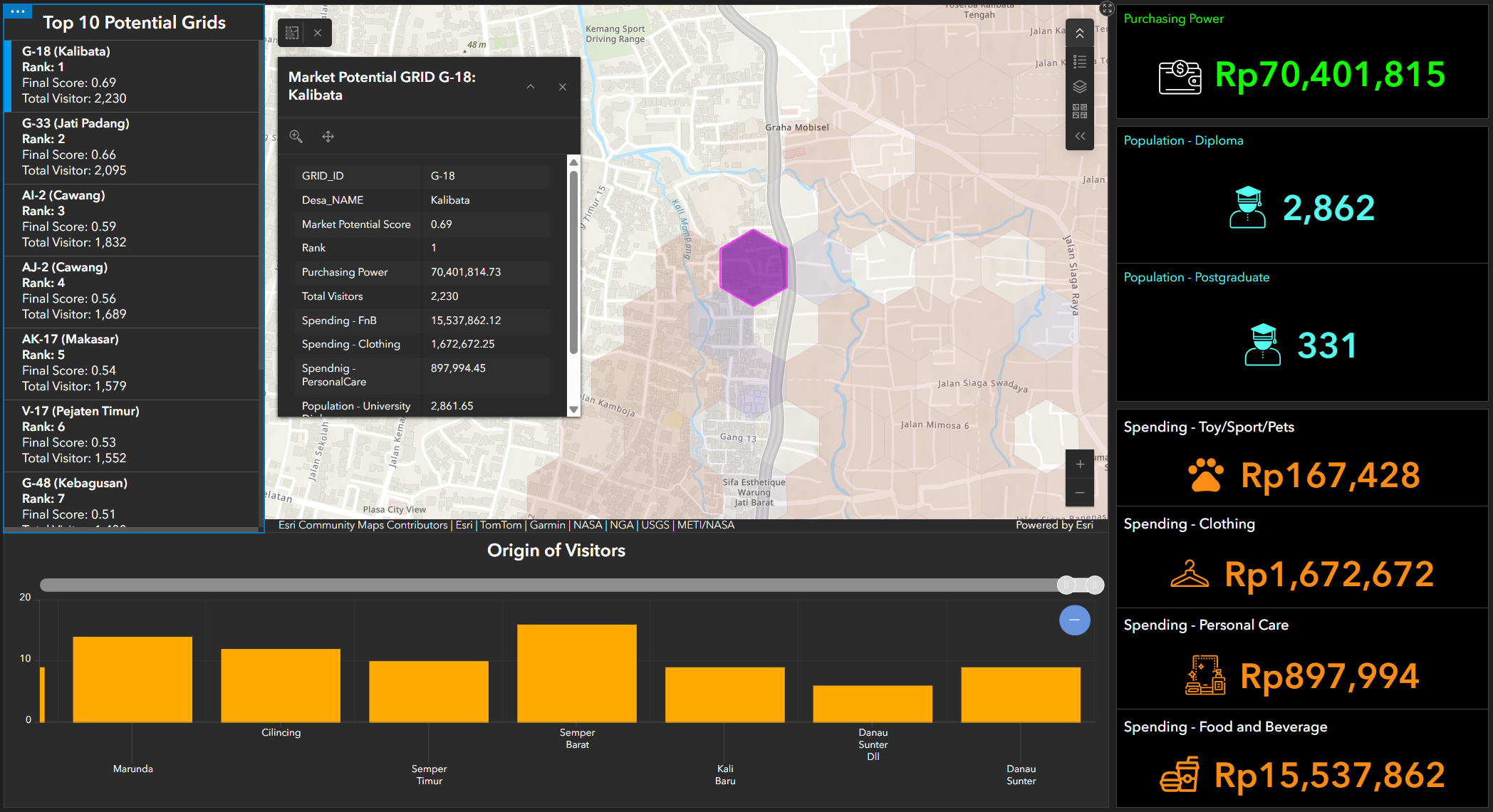

Hyperlocal market segmentation

- Distribution optimization: Align branch or agent placement with high-potential clusters integrating contextual market data such as people movement and sociodemographic.

- Tailored product offerings: Create tailorized products and services schemes based on local sociodemographic dynamics.

- Precision marketing: Target campaigns at the grid level, not just city-wide.

This allows banks to expand financial inclusion more responsibly, address literacy gaps and compete more effectively with trending fintechs growth.

Without GIS, banks face three critical risks:

- Underestimating disaster exposure, leading to sudden spikes in loan defaults

- Weak NPL monitoring, resulting in unsustainable lending programs

- Overlooking hyperlocal opportunities, allowing fintechs to capture underserved markets

In Indonesia’s competitive and risk-prone environment, ignoring GIS is not merely a missed opportunity; it is a strategic vulnerability that can undermine resilience and long-term growth.

How ArcGIS empowers banks

GIS platforms like Esri’s ArcGIS enable banks to:

- Enrich core banking systems with spatial context and insights

- Visualize risk exposure in real time

- Automate asset monitoring with geo-tagging

- Deliver hyperlocal insights to gain competitive advantage

From mapping to intelligence: The ArcGIS advantage

By moving from ’maps’ to decision intelligence, banks unlock a new level of resilience, precision and growth.

For Indonesian banking leaders, the message is clear. GIS is no longer optional - it is a strategic imperative for risk management, NPL control, and market expansion. By embedding location intelligence into decision-making, banks can safeguard portfolios, serve communities responsibly, and outpace competitors.

In Indonesia, future banking performance will be defined not just by financial metrics but also by how effectively institutions use location intelligence. Those who act now will lead; those who delay risk being left behind.

Discover more ArcGIS capabilities for the banking sector. Contact our specialist.